Economic & Market Overview - June

Global

The trade war between the United States and China took a turn for the worst when President Trump announced an increase (from 10% to 25%) on $200bn worth of Chinese goods early in May. There are a few other geo-political matters that are causing market participants to be jittery, but the US-China relations remain the biggest contributor to the recent increase in market volatility.

According to BCA Research, political developments ahead of the 2020 US Presidential election are also adding to uncertainty in the investment outlook. The Democratic Primary race will heat up in June and President Trump, while favoured in 2020 (barring a recession), is currently lagging both Joe Biden and Bernie Sanders in the head-to-head polling. Trump’s legislative initiatives are bogged down in gridlock and scandal. The remaining avenue for him to achieve policy victories is foreign policy – hence his increasing aggressiveness on both China and Iran.

The result is negative sentiment toward global risk assets in the near term and, possibly, also for the next few years. A positive catalyst is desperately needed in the form of greater stimulus to the Chinese economy (which has a high likelihood) and significant progress toward a trade agreement between the world’s two largest economies. Against this backdrop, Brexit, Italy, and European risks pale by comparison. Nevertheless, the odds of Brexit actually happening are on the rise. The uncertainty will weigh on sentiment in Europe through the current due date of 31 October even if it does not ultimately conclude in a no-deal shock that prevents the European economy from bouncing back. UK Prime Minister Theresa May’s resignation has hurled the Conservative Party into a scramble to select her successor. While the timeline for this process is straightforward, the impact on the Brexit process is not. The odds of a “no-deal Brexit” have increased but so has the prospect of parliament passing a soft Brexit prior to any new election or second referendum. Untangling from the European Union proved to be far more complex than what most lawmakers expected. With emerging markets also struggling in the face of a slowing global economy, there will be limited opportunities for global multi-asset portfolios, with both bonds and equities forecast to generate below-average returns in the next decade.

South Africa

At the recent meeting of the South African Reserve Bank’s Monetary Policy Committee South Africa’s growth outlook has been revised downwards, given the poor start to 2019. RMB Global Markets now expect the local economy to grow by 0.7% in 2019. This is still be well behind the global average of in excess of 3% in real terms. Many emerging markets are still growing at over 5% per annum – a growth rate that South Africa requires to structurally address its high unemployment rate. There are several contributing factors to the most recent downward revision, but it will have been heavily influenced by electricity supply constraints. The South African consumer is coming under pressure with higher petrol and electricity prices in a subdued economic growth environment. Rising unemployment figures and an increasing tax burden are further factors weighing on consumers this year. In addition, the FNB/BER Consumer Confidence Index fell to 2 points in 1Q19, sitting at its long-term average. Household consumption is expected to be subdued during 2019. Concerns are rising that demand for credit by higher income consumers is being used to maintain their current lifestyles. This is likely to lead to the continued increase in the ratio of household debt to disposable income that has been on an upward trend since the beginning of 2018 – a very dangerous development in a low growth environment. There is a silver lining though – inflation seems to be under control, and this could lead to a reduction in official interest rates. Some local economists are calling for a drop of up to 2% (which they argue can easily be justified) in order to give the South African economy a much-needed boost, but the next move is unlikely to be as dramatic even if it is in the right direction.

Market performance

Alongside the increase in geo-political risks mentioned above, uncertainty around slowing global economic growth and concerns relating to sluggish global trade, translated into investors preferring safe haven assets such as US Treasuries over risky assets. The yield on the US 10-year Treasury fell to its lowest level in almost two years and the US Treasury index recorded a 2.4% return for the month (in US Dollars).

Local bonds also ended the month higher (up 0.6% in local currency terms) but most other asset classes pulled back during the month of May. Global equities gave up 4.4% (in rand terms) and the FTSE/JSE All Share index ended the month 4.8% lower. Resources (-5.1%) and industrials (-6.0%) were the big losers, while financials (-2.3%) and listed property (-0.9%) weathered the storm a little better. Two thirds of the top 60 stocks ended in the red, and heavyweights like British American Tobacco (-9.0%), Naspers (-10.4%) and Sasol (-22.7%) all gave up significant gains from the start of the year.

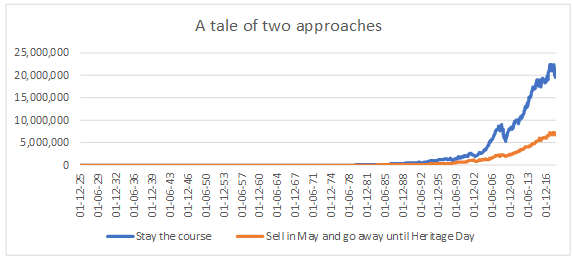

Commentary – Sell in May and go away During May, most asset classes – locally and abroad – gave up much of the gains from the first quarter’s relief rally in growth assets. It led to many investors referring to the rule of thumb “sell in May and go away.” This month we look at how well this approach would have worked for investors in the South African equity market over the last few decades. The complete phrase has its origins in the City of London. "Sell in May and go away and come on back on St. Leger's Day" refers to a custom of bankers, merchants and aristocrats who would spend their (sometimes even warm and sunny) summers in the English countryside, away from the hustle and bustle of the markets. St Leger’s Day refers to the St Leger’s Stakes – a thoroughbred horse race held in the first half of September since 1776. In the United States, a localised interpretation of this phrase refers to the period between Memorial Day (the last Monday in May) and Labour Day (the first Monday in September). Since 1994 a South African interpretation could refer to the period between Worker’s Day (1 May) and Heritage Day (24 September). “Sell in May and come on back after Heritage Day”. It has a nice ring to it, doesn’t it? Let’s see how this strategy would have worked over the last 90 or so years when we analyse the total return of the FTSE/JSE All Share Index since 1926. The average annual return (from 1926 to 2018) of an investment in the South African stock market was 14.2% per annum. Very few investors would live long enough to reap the rewards of their persistence but if you invested R100 on 1 January 1926 you would have had nearly R20.5 million on 31 December 2018. Patience turned out to be a virtue after all! If the same investor chose to disinvest on 30 April every year and returned to the market at the end of September, the total annual growth rate would have changed from 14.2% per annum (for remaining fully invested) to only 12.3% per annum. This would have changed your fortune of more than R20 million into only R7 million. If you kept the money under your mattress from May to September (instead of entrusting a bank to look after it) your return would have been only one sixteenth of this – a paltry R432 000!

It’s clear that this approach would not have worked over the very long term. In hindsight, remaining invested would have been the winning strategy by some margin. A more realistic analysis would be to consider this approach over rolling ten-year periods – a much more sensible horizon for equity investors. This is where it starts to get interesting. Of the 84 rolling ten calendar year periods “Sell in May and go away” would actually have worked 42% of the time. Not quite an even chance, but much better than before. It is, however, important to consider the margin of outperformance. When “remaining invested” did better than “Sell in May”, it outperformed, on average, by 5.7% per annum. In the 42% of instances where “Sell in May” worked better, it outperformed by only 4.1% per annum on average. In summary: remaining invested works more frequently than following some rule of thumb that originated in a foreign market far from here. And when the former works, it also has better results on average. Let’s pray that it also holds true for President Ramaphosa’s new cabinet…

Source : APS Monthly Economic Commentary